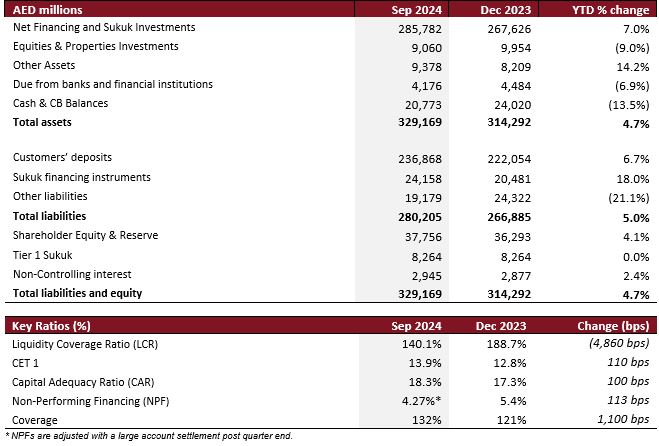

- Balance Sheet expands to AED 329 billion, up almost 5% YTD.

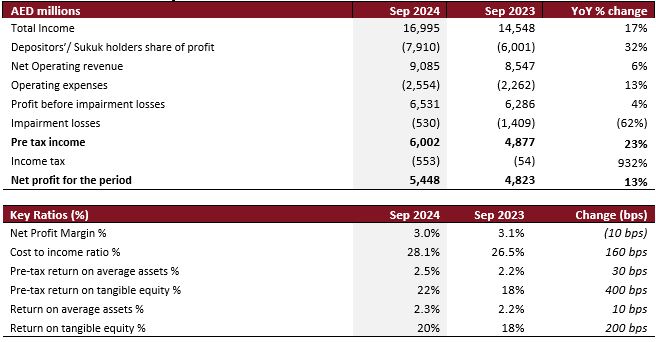

- Strong growth in Total Income by 17% YoY to AED 17 billion.

- Pre-Tax Profit of AED 6 billion, a robust growth of 23% YoY.

- Upgrade in the bank’s Viability Rating (VR) to ‘bbb-’ from ‘bb+’, from Fitch Ratings.

- Upgrade in the bank’s MSCI ESG Rating to ‘A’ from ‘BBB.’

Dubai Islamic Bank (DFM: DIB), the largest Islamic bank in the UAE, today announced its results for the period ending September 30, 2024.

9M 2024 Highlights:

- Group Pre-Tax Profit registered AED 6,002 million up 23% YoY, while Group Net Profit came in at AED 5,448 million, up 13% YoY. 3Q 2024 Pre-Tax Profit is AED 2,281 million up 32.1% YoY.

- Net financing and sukuk investments reached AED 286 billion, up 7% YTD. Net financing growth picked up on a YTD basis at 3.7%. Gross new underwriting and sukuk investments recorded AED 68.8 billion in 9M 2024.

- Total income reached AED 16,995 million compared to AED 14,548 million, a solid expansion of 16.8% YoY.

- Net Operating Revenues showed a robust increase of 6.3% YoY to reach AED 9,085 million.

- Group Net Profit stood at AED 5,448 million, a 13.0% YoY increase compared to AED 4,823 million in 9M 2023.

- Balance sheet rose by 4.7% YTD to reach AED 329 billion.

- Customer deposits increased to AED 237 billion, up 6.7% YTD with CASA deposit contributing over 38.1%, up more than 150 bps from 36.6% at the beginning of the year.

- Impairment charges came at AED 530 million, significantly declining by 62% YoY against AED 1,409 million in 9M 2023.

- NPF improved to 4.27% compared to 5.40% in YE 2023, lower by 113 bps YTD. Cash Coverage now at 97%.

- Cost to income ratio up by 160 bps YoY to 28.1%, as the bank continue to strengthen its key areas and functions in line with its growth strategy.

- LCR remains robust at 140.1%.

- ROA is stable at 2.3% while ROTE to 20% up 200 bps YoY. Pre-tax RoA and RoTE at 2.5% and 22% respectively.

- CET1 at 13.9% (+110 bps YTD) and CAR at 18.3% (+100 bps YTD), denotes a well-capitalized entity to leverage growth opportunities.

- Fitch Ratings has upgraded the bank’s Viability Rating (VR) to ‘bbb-‘ from ‘bb+’, citing the DIB’s improved asset quality metrics coupled with the bank’s solid business, earnings and funding profiles.

Management’s comments for the period ended 30th September 2024:

His Excellency Mohammed Ibrahim Al Shaibani, Director-General of His Highness The Ruler’s Court of Dubai and Chairman of Dubai Islamic Bank

- The UAE continues its robust progress towards economic growth & development despite global uncertainties and regional conflicts. With inflation now showing signs of moderation, central banks have now embarked on lowering rates generating more favorable financial market and economic conditions. UAE’s growth projections remain amongst the strongest in the region driven by rising population, growing tourism and enhanced trading volumes.

- Accordingly, DIB’s nine-month performance has been remarkable with total income of nearly AED 17 billion, a robust 17% YoY rise. The bank continues to secure strong new origination from our growing customer base across the country and the region at large.

Dr. Adnan Chilwan, Group Chief Executive Officer

- A strong nine-month performance for the bank with Group profit (pre-tax) of AED 6 billion up 23% YoY, supported by improving operating conditions and continued strong underwriting on new business. Return ratios continue to improve with RoA at 2.3% (+10 bps YoY) and RoTE at 20% (+ 200 bps YoY).

- The UAE banking system remain robust despite the global market and regional volatilities as exhibited by rising lending as well as deposit volumes. The strong performance of the sector is driven by a positive economic outlook with increasing business activities, improving asset quality, as well as rising profitability.

- All business units achieved positive performance with both corporate and consumer portfolios adding new net lending of more than AED 7 billion across several sectors. Along with a solid growth in the fixed income book, the bank’s financing and sukuk portfolio reached AED 286 billion, up 7% beating year end guidance by 180 bps.

- The recent upgrade of the bank’s viability rating is a clear demonstration of our persistent efforts to protect and grow the franchise across strengthening key areas such as asset quality, earnings, capital as well as funding & liquidity.

- DIB earned significant improvements with several of its external ESG ratings, including from some of the top raters such as MSCI which has recently upgraded DIB to “A” from “BBB.” The Bank has been recognized for both making progress against its ESG strategy, and for enhancing disclosures and increasing transparency in our sustainability reporting.

Financial Review

Income statement summary

Balance Sheet Summary

Operating Performance

The bank’s Total Income rose to AED 16,995 million in 9M 2024 demonstrating a solid growth of 16.8% YoY compared to AED 14,548 million. Non-funded income advanced by 32% YoY over the reporting period supported by income from investment properties, properties held for sale, other income and associate income. Net Operating Revenue grew by 6.3% YoY to reach AED 9,085 million compared to AED 8,547 million last year.

Pre-impairment profit increased by 3.9% YoY reaching AED 6,531 million compared to AED 6,286 million. Impairment charges stood at AED 530 million down by a significant 62.4% YoY.

Operating expenses amounted to AED 2,554 million for the year vs AED 2,262 million in 9M 2023, exhibiting 12.9% YoY increase. Cost income ratio registered 28.1%, up 160 bps YoY.

Pre-tax profit grew by 23.1% YoY to reach AED 6,002 million. Despite the introduction of corporate tax, Group Net Profit increased by 13.0% YoY to reach AED 5,448 million vs AED 4,823 million in 9M 2023.

Net profit margin stable at 3.0%. Separately, post tax ROA is stable at 2.3% while ROTE stands at 20%. Pre-tax ROA and ROTE stood at 2.5% and 22% respectively.

Balance Sheet Trends

Net financing & Sukuk investments stood at AED 286 billion, up 7% YTD from AED 268 billion in FY 2023.

DIB witnessed strong gross new underwriting of 22% YoY in the consumer portfolio during the 9M 2024 period to AED 19 billion. Similarly, the bank’s corporate net new underwriting added AED 2 billion despite being impacted by AED 17 billion of early settlements. This contributed to the bank’s financing portfolio growth over the 9M 2024 period to AED 206.8 billion, up 3.7%.

Customer deposits registered AED 237 billion up by 6.7% YTD. CASA reached AED 91 billion up 11% YTD and comprising 38% of deposits. Investment deposits contribution remained stable at 62%. Liquidity coverage ratio (LCR) at 140.1%, remains above regulatory requirement, depicting strong liquidity position.

Non-performing financing (NPF) ratio improved to 4.27%, down by 113 bps compared to FY 2023. The NPF absolute amount decreased by 18.5% from AED 11.5 billion during YE 2023 to AED 9.36 billion. NPFs are adjusted with a large account settlement post quarter end.

Stage 1 financing is up by 5% to AED 192 billion while Stage 2 financing ended the period at AED 12.5 billion down 13% due to some accounts moving to stage 1. Similarly, Stage 3 coverage is stable at 67.1% as stage 3 exposure dropped to over AED 9 billion, the lowest level over the past 3 years.

Cash coverage ratio now stands at 97% and overall coverage including collateral at 132%. Cost of risk came in at 26 bps compared to 57 bps in FY 2023.

Capital ratios continue to remain strong with CAR at 18.3% and CET 1 ratio at 13.9%, both well above the regulatory requirement.

Business Performance (9M 2024)

Consumer Banking portfolio reached AED 61 billion up 9% YTD. The portfolio’s total new underwriting of AED 19.5 billion during the year increased from AED 16 billion, up 22% YoY. All consumer segments particularly credit cards and auto finance were up by 23% and 17% on a YTD basis. Despite routine repayments of AED 14.4 billion, the portfolio added nearly AED 5.1 billion of net new underwriting in 9M 2024 versus AED 3.1 billion in 9M 2023. Blended yield on consumer financing grew by 33 bps YoY to reach to 7.0%. Separately, on the funding side, consumer deposits increased by 2% YTD to AED 90 billion while consumer CASA remained sticky at AED 46.8 billion.

Corporate banking portfolio reached AED 145.6 billion up 3% YTD. Revenues increased by almost 5% YoY to AED 2.2 billion. Yield on corporate financing portfolio expanded by 30 bps YoY to 6.7% compared to 6.4% during 9M 2023. On the funding side, corporate deposits increased by 11% on a YTD basis while CASA advanced by a healthy rate of 28% YTD, as the bank continued to attract strategic corporate clients.

Treasury continued to provide a strong engine for growth as the curator of the bank’s fixed income book. The sukuk investment portfolio now stands at AED 79 billion, up a solid 16% YTD. Having said that, net new sukuk investments during the year amounted to AED 16 billion. The portfolio carries an attractive yield of 4.8% up 18 bps YoY.

Key Highlights (Q3 2024)

- Fitch Ratings has affirmed Dubai Islamic Bank's Long-Term Issuer Default Rating (IDR) at 'A' with a Stable Outlook. Fitch has also upgraded the bank's Viability Rating (VR) to 'bbb-' from 'bb+'. This reflects DIB's improved asset-quality metrics, stronger risk management as well as strong earnings and funding profiles. The improved VR rating demonstrates the strengthening financial and credit position of the bank supported by improving operating conditions of the UAE.

- Dubai Islamic Bank led the landmark $3.25 Billion financing transaction for GEMS Education. The bank played a pivotal role in spearheading the facility for GEMS Education, the largest private K-12 education provider in the world. This transaction underscores DIB's leadership in the financial sector, particularly in structuring and underwriting significant deals that foster growth and development in key industries. The multi-billion-dollar, sustainability linked facility was underwritten by a UAE bank consortium led by DIB.

- The bank provided financial support towards the development of the Hamdan Bin Rashid Cancer Hospital, with a substantial pledge to healthcare in Dubai with an AED15 million contribution to Al Jalila Foundation, which leads the Giving mission of Dubai Health. The contribution will support the development of Dubai Health’s Hamdan Bin Rashid Cancer Hospital, the first comprehensive cancer care hospital in Dubai, underscoring their commitment to the community’s well-being and advancing healthcare infrastructure.

- DIB signed an MOU with Mohamed bin Rashid Fund to empower UAE National-Owned SMEs. The bank, signed an MOU with the Mohamed bin Rashid Fund for the Support of Small and Medium-Sized Enterprises, represented by His Excellency Abdulbaset Al Janahi, CEO of Dubai SME. This partnership aims to provide Sharia-compliant strategic financing solutions through a Credit Guarantee Scheme to empower UAE National-owned SMEs.

- The bank successfully achieved significant upgrades and increases in most of its ESG scores & ratings. This move by external agencies indicates robust progress on the ESG agenda and significantly enhance transparency via public disclosure.

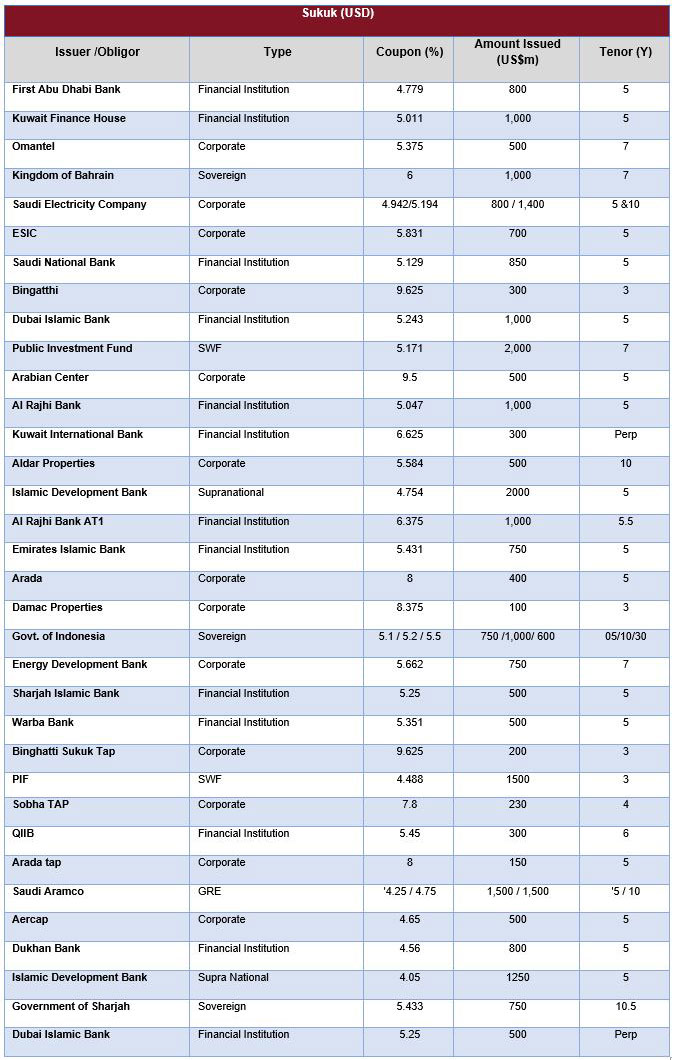

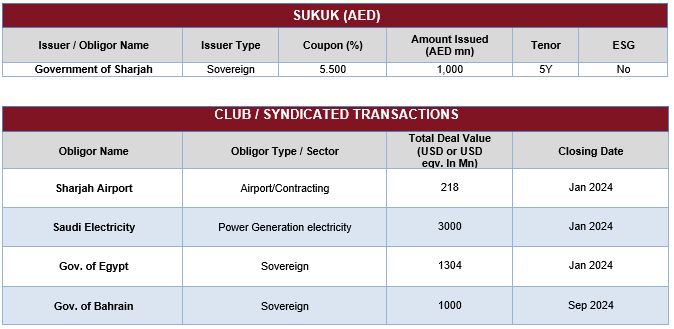

DCM and Syndication Deals (9M 2024)

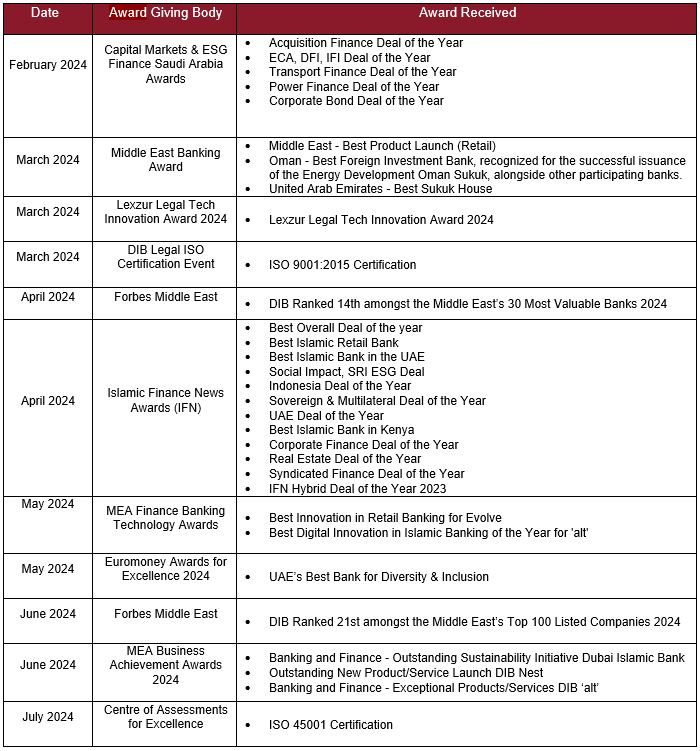

Awards List (9M 2024)