Dubai Islamic Bank (DFM: DIB), the largest Islamic bank in the UAE, today announced its results for the period ending September 30, 2023.

9M 2023 Highlights:

Management’s comments for the period ending 30th September 2023:

His Excellency Mohammed Ibrahim Al Shaibani, Director-General of His Highness The Ruler’s Court of Dubai and Chairman of Dubai Islamic Bank

Dr. Adnan Chilwan, Group Chief Executive Officer

Financial Review:

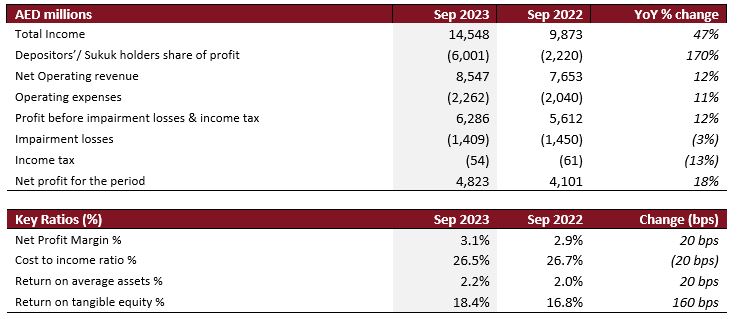

Income statement summary

Balance Sheet Summary

Operating Performance

The bank’s Total Income rose to AED 14,548 million in 9M 2023 demonstrating a notable YoY growth of 47% compared to AED 9,873 million primarily driven by strong income from financing assets and non-funded income. Non-funded income advanced by 15% YoY over the reporting period supported by fees & commissions and income from investment properties in line with Dubai’s strong property rental market. Particularly 3Q 2023 non funded income exhibited a strong quarter YoY up by 49% as commissions rose by 17% due to higher financing processing fees and rental income. This is clearly reflected in the Net Operating Revenue which grew by 12% YoY to reach to AED 8,547 million compared to AED 7,653 million last year.

Pre-impairment profit increased by 12% YoY reaching to AED 6,286 million compared to AED 5,612 million. Impairment charges stood at AED 1,409 million down by 3% YoY. Additionally, 3Q 2023 charges exhibited a declining trend both YoY and QoQ by 10% and 3% respectively.

Operating expenses amounted to AED 2,262 million during 9M 2023 vs AED 2,040 million in 9M 2022, exhibiting 11% YoY increase. Cost income ratio improved to 26.5%, down 20 bps YoY.

Group Net Profit witnessed a robust increase of 18% YoY to reach AED 4,823 million vs AED 4,101 million in 9M 2022. 3Q 2023 net profit registered AED 1,713 million up 6.7% QoQ and 22% YoY.

Net profit margin increased to 3.1% (+10bps YoY) with ROA and ROTE at a healthy 2.2% and 18.3% up by 20 bps and 130 bps YTD respectively.

Balance Sheet Trends

Net financing & Sukuk investments stood at AED 265 billion, up 11.3% YTD from AED 238 billion in FY 2022. DIB’s net financing assets were up by 7% YTD while the Sukuk investments portfolio, another key focus of the bank, expanded by nearly 27% YTD (+8% QoQ) to reach to AED 66 billion.

DIB witnessed stellar overall YoY growth in gross new financing and sukuk during 9M 2023 amounting to nearly AED 72 billion, up 69% compared to AED 43 billion in 9M 2022. The bank’s sukuk portfolio continued its resilience witnessing gross new investment of AED 19 billion doubling YoY compared to 9M 2022 eventually leading to net growth of AED14 billion. Separately, gross corporate financing origination surpassed AED 37 billion, (+ 85% YoY), driven mainly by large corporates and regional cross border financing, while new bookings from consumer financing followed suit up 21% to AED 16 billion driven by automotive and personal finance, underpinning DIB’s strong franchise despite a competitive market. Routine repayments for the period continued to flow in at AED 18 billion and AED 13 billion from the corporate and consumer segments respectively. The momentum of early settlements has retracted over the period by 23% YoY to AED 10 billion compared to AED 13 billion last year. This has resulted in net positive financing incremental growth of AED 13 billion in DIB’s portfolio over the 9M 2023 period compared to balanced growth last year. On a YoY basis, 3Q 2023 gross new underwriting grew five folds, coupled with significantly lower early settlements compared to the same quarter last year, resulting in a positive net growth of AED 9.5 billion.

Customer deposits stood at AED 221 billion as of 9M 2023 up by 11.2% YTD equally supported by the consumer and corporate accounts. CASA now stands at AED 82 billion, comprising 37% of deposits. Migration to wakala deposits continued during the period due to the current global rate scenario. This is reflected through an increase in the wakala structure (investment deposits) which is up 24% YTD. Liquidity coverage ratio (LCR) at 166%, up from 150% FY 2022, remains above regulatory requirement, depicting strong liquidity position.

Non-performing financing (NPF) ratio improved to 6.04%, down 42 bps compared YE 2022. Recoveries from NMC and NOOR POCI are ongoing which resulted in a decline of 11% in their NPF exposure. Accordingly, NMC’s coverage ratio increased by 600 bps YTD to 80% and by 1100 bps to 39% for the NOOR POCI account. Finally, core DIB NPF account witnessed a slight 1.2% uptick on a YTD basis (flat QoQ) to AED 10.9 billion well covered at 87% (up +400 bps YTD).

Stage 2 financing increased by 18% YTD to AED 18 billion, flat QoQ due to normal flow between stages. Stage 2 coverage ratio improved to 7.4% recovering to YE levels and also 70 bps up QoQ. On the other hand, Stage 3 coverage accordingly improved to 65.4%, (+420 bps) from FY2022 on the back of intensive efforts on recoveries.

Cash coverage ratio improved to 83% (+600 bps YTD, +800 bps vs 9M 2022) and overall coverage including collateral at 117% (+700 bps YTD and 1,200 bps vs 9M 2022). Cost of risk on gross financing assets stood at 71 bps compared to 84 bps for the year 2022, an improvement of 13 bps YTD.

Capital ratios continue to remain strong with CAR now at 18.1% (up 50 bps YTD) and CET 1 ratio at 13.6% (up 70 bps YTD), both well above the regulatory requirement.

Business Performance (9M 2023)

Consumer Banking portfolio stood at AED 54 billion up 4% from AED 52 billion in FY2022. The portfolio’s total new underwriting of AED 16 billion during the period increased from AED 13 billion in 9M2022, up 21% YoY. In this, all consumer segments witnessed strong growth particularly auto finance which featured a 34% jump YoY and Personal Finance up 20% YoY in gross new underwriting. Despite routine repayments of AED 13 billion, the portfolio grew by AED 3 billion over the 9M 2023 period. The business generated AED 3.7 billion in revenues during the year up a hefty 24% YoY from AED 3 billion during 9M 2022. Blended yield on consumer financing grew by 85 bps YoY to reach to 6.7%. Separately, on the funding side, consumer deposits witnessed an 11% increase YTD to AED 87 billion as investment deposits gained traction from customers while consumer CASA remained steady YTD at AED 48 billion.

Corporate banking portfolio now stands at AED 145 billion up 8.2% YTD driven by growth in the services, automobile and financial institution sectors. Gross new corporate financing for 9M 2023 bolstered to AED 37 billion up 85% YoY, while repayments and early settlements registered AED 27 billion, leading to AED 10 billion growth in the portfolio over the 9M 2023 period. This growth features a robust recovery in the corporate portfolio as the bank’s strong liquidity position enabled it to deploy financing strategically, coupled with a drop in early settlement. Revenues featured double digit growth reaching AED 3.4 billion, up 29% YoY compared to AED 2.7 billion in 9M 2022. Yield on corporate financing portfolio expanded by 300 bps YoY to 6.38% compared to 3.39%. Separately on the funding side, corporate deposits increased by 10% YTD while CASA was impacted by 8% YTD as large corporates continued to rotate their funds into higher yielding deposits.

Treasury continued to provide strong impetus to growth as the custodian of the bank’s fixed income book. The sukuk investment portfolio now stands at AED 66 billion, up 26.8% YTD, constituting a significant 21% of the bank’s assets. Gross new sukuk investments during the 9M 2023 amounted to AED 19 billion doubling YoY, leading to net growth of AED 14 billion for the period. The portfolio carries an attractive yield of 4.61% up 65 bps YoY.

Key Business Highlights (Q3 2023)

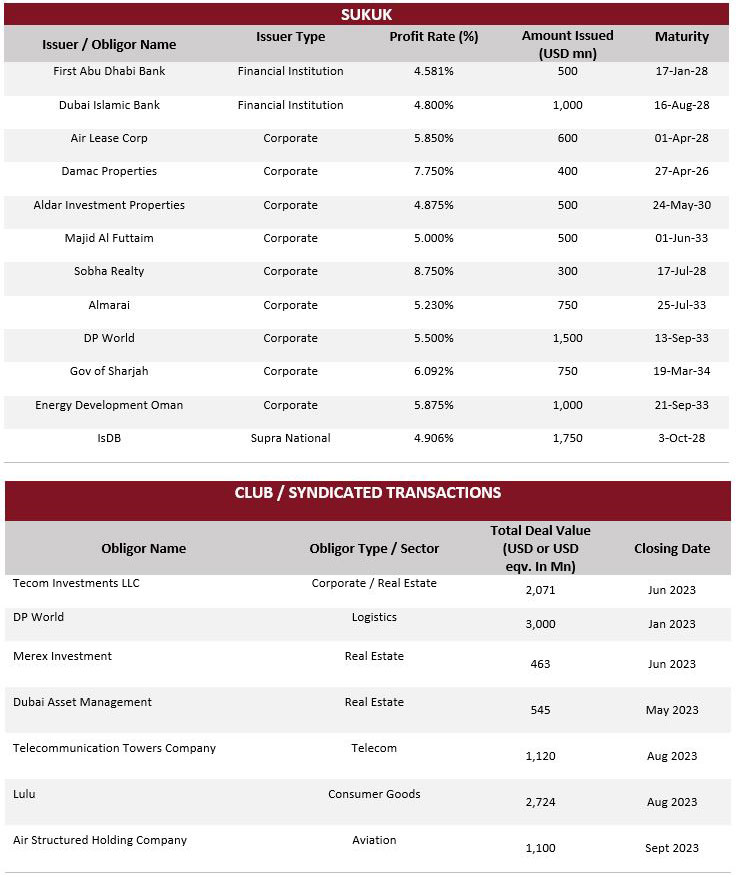

DCM and Syndication Deals (2023 YTD)

Awards List (2023 YTD)

DIB Successfully Issues Debut Sustainability-Linked Financing Sukuk

DIB and HCLTech Forge Strategic AI Innovation Partnership