- Significant increase in profitability of 45% YoY to reach to AED 2.7 billion.

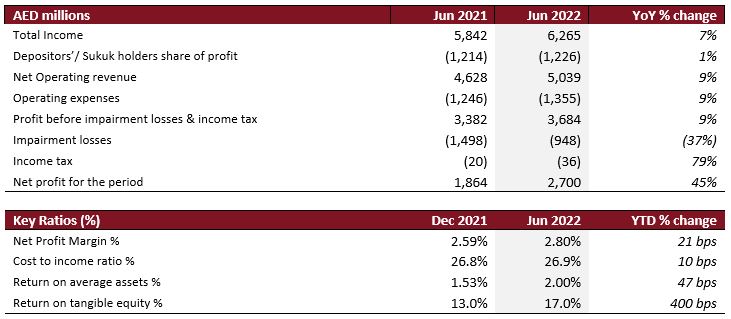

- Substantial rise in total income by more than 7% YoY to AED 6.3 billion.

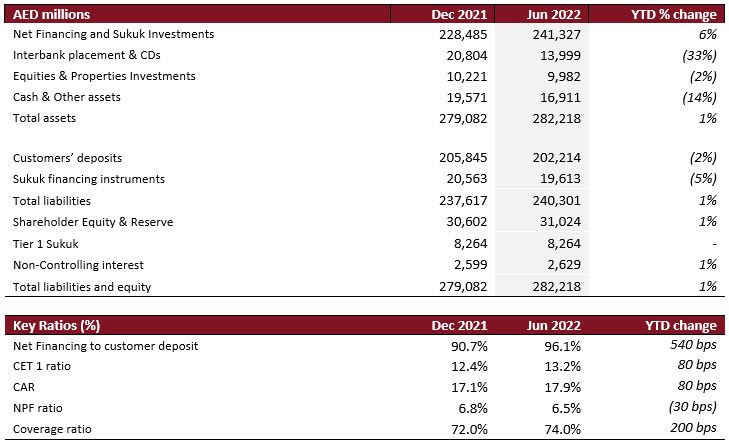

- Strong growth on core assets of 6% YTD to reach to AED 241.3 billion.

- Strong underlying performance has led to upward revisions on 2022 guidance metrics

Dubai Islamic Bank (DFM: DIB), the largest Islamic bank in the UAE, today announced its results for the period ending June 30, 2022.

First Half 2022 Highlights:

- Substantial growth in Group Net Profit of 45% YoY to AED 2,700 million vs AED 1,864 million in same period last year. The strong growth was driven by rising core revenues and sustained lower impairments.

- Gross new financing and sukuk investments saw a remarkable increase by AED 33 billion during the period. Excluding regular repayments and maturities, the bank saw an incredible AED 20 billion growth.

- Net financing and sukuk investments grew by 6% YTD to AED 241.3 billion compared to AED 228.5 billion in 2021 indicating a strong rebound in 2022, despite regular repayments and sukuk settlements of AED 13 billion as well as early repayments of AED 7 billion.

- Net Operating Revenues showed a robust growth of 9% YoY and 4% sequentially to reach AED 5,039 million.

- Total income reached to AED 6,265 million compared to AED 5,842 million, substantially up by 7% YoY and 8% sequentially.

- Net Operating Profit now at AED 3,684 million, a strong increase of 9% compared to AED 3,382 million in H1 2021.

- Balance sheet remains robust at AED 282.2 billion, up 1% YTD.

- Customer deposits now at AED 202.2 billion with CASA comprising 44% of the deposit base.

- Significantly lower impairments of AED 948 million against AED 1,498 million in previous year, down by 37% YoY, demonstrate continued improvement in asset quality.

- NPF ratio continues its downward momentum now at 6.5% lower by 30bps YTD compared to 6.8% in 2021.

- Cost to income ratio amongst the best at 26.9%, lower by 140bps sequentially.

- Liquidity remains healthy with finance to deposit ratio of 96% and LCR of 117%.

- Continued healthy improvement on ROA now at 2.0% up by 47bps YTD and ROTE at 17.0% up by 400bps YTD.

- Capitalization levels remain robust with CET1 at 13.2% (+80bps YTD) and CAR at 17.9% (+80bps YTD), both well above the minimum regulatory requirement. Total equity now stands at AED 41.9 billion.

Management’s comments for the period ending 30th June 2022:

His Excellency Mohammed Ibrahim Al Shaibani, Director-General of His Highness The Ruler’s Court of Dubai and Chairman of Dubai Islamic Bank

- Global growth has been moderate during the first half of the year due to events that have led to trade and supply chain disruptions. Despite these occurrences, the GCC region and the UAE remain strong building on the economic foundations and reforms implemented earlier. Dubai’s progressive economic recovery remains on track and DIB’s momentous first half results reflect the improving macro economic conditions.

- With a comprehensive and integrated sustainability strategy, the bank is fully aligned towards the vision of the UAE President and is committed towards enhancing the nation’s economic competitiveness, while simultaneously advancing the sustainability objectives of the country.

- Despite global headwinds, the bank’s total income rose strongly by 7% YoY to more than AED 6.3 billion. This clearly demonstrates the bank’s robust fundamentals and the strength of the balance sheet to navigate the uncertainties in the market.

Dr. Adnan Chilwan, Group Chief Executive Officer

- Another remarkable set of results with net profit reaching AED 2.7 billion, a 45% YoY rise, on the back of a strong economic rebound. This significant jump primarily stems from core business growth with net operating revenues rising by 9% YoY and 4% QoQ to AED 5 billion, while a fall in the impairments charges by 37% YoY reflects the fast improving asset quality.

- The improving profitability trend has had a positive impact on shareholder returns with ROA now at 2% (+47bps YTD) and ROTE at 17% (+400bps YTD).

- Our net financing and sukuk investments expanded strongly by nearly 6% YTD to reach AED 241 billion supported by increasing volumes across all businesses. The first 6 months have already seen new gross financing and sukuk investments to the tune of AED 33 billion, and normal repayments and early settlements aside, we are left with AED 13 billion of growth, which is remarkable achievement.

- The bank’s asset quality has continued to improve sequentially over the past few quarters with a 30bps YTD improvement in NPF ratio which now stands at 6.5%. The bank remains persistent in its efforts to strengthen credit underwriting and manage asset quality with a proactive and cautious approach to growth amidst the current operating environment. Consequently, the declining cost of risk now down to 76bps further evidences the success of the strategy.

Financial Review:

Income statement summary

Balance Sheet Summary

Operating Performance

The bank’s total income rose to AED 6,265 million in H1 2022 demonstrating a robust growth of 7% YoY compared to AED 5,842 million in same period of last year following strong recoveries in business volumes. This is clearly reflected in the Net Operating Revenue which saw an uptick of 9% YoY to reach to AED 5,039 million compared to AED 4,628 million last year.

Pre-impairment profit during the 1st half increased by 9% YoY reaching to AED 3,684 million compared to AED 3,382 million. The bank’s constant focus on prudent risk management resulted in significantly lower impairment charges amounting to AED 948 million vs AED 1,498 million last year, an improvement of 37% YoY.

Operating expenses amounted to AED 1,355 million during H1 2022 vs AED 1,246 million in H1 2021 exhibiting a 9% YoY increase. The rise in expenses is attributed to the strengthening of resources within the key control and support functions of the bank as well as continued investment in systems and operational infrastructure of the bank.

Following higher revenue growth, cost income ratio now stands at a sector leading position at 26.9%. Digital continuous to deliver strong performance sequentially across all key metrics with on-going releases of new services and enhancements catering to the large and growing customer base.

As a result, the bank’s Group Net Profit witnessed a significant rise of 45% YoY to reach AED 2,700 million vs AED 1,864 million in H1 2021.

Net profit margin increased to 2.8% (+21bps YTD) with ROA and ROTE at a healthy 2% and 17% respectively.

Balance Sheet Trends

The first half performance clearly highlights the robustness of the bank’s growth engine which effectively saw gross new financing and sukuk investments of AED 33 billion. The bank witnessed a strong growth in new financing of over AED 26 billion YTD driven by robust growth in gross corporate new financing of nearly AED 17 billion and gross consumer financing of AED 9 billion during the first half of 2022. Sukuk investments saw a robust increase of AED 7 billion, up by 12% YTD to reach AED 47 billion driven by continued focus on growing this highly profitable portfolio. Considering normal repayments and maturities, the portfolio grew by AED 20 billion, a significant achievement despite market volatilities.

Given the above, net financing & Sukuk investments rose by a substantial 6% YTD to reach at AED 241.3 billion from AED 228.5 billion in 2021.

Customer deposits stood at AED 202.2 billion at the end of H1 2022 with CASA now standing at AED 89.4 billion representing 44% of deposits. The stability of CASA book despite rising rates clearly highlights the strength of DIB’s liquidity strategy. Liquidity coverage ratio (LCR) at 117% remains well above regulatory requirement with finance to deposit ratio of 96.1%, both depicting a healthy and comfortable liquidity position.

Credit quality showcases a clearly trend with non-performing financing (NPF) ratio seeing a decline of 30bps YTD to 6.5%. The above has led to Cash coverage ratio increasing to 74% (+200 bps YTD) and overall coverage including collateral at 103% (+100bps YTD). Cost of risk on gross financing assets now stands at 76 bps compared to 99 bps for the year 2021, an improvement of 23 bps YTD.

Capital ratios continue to remain strong with CAR now at 17.9% and CET 1 ratio at 13.2%, both well above the regulatory requirement.

Key Business Highlights H1 2022

- DIB became the first Islamic bank in the UAE to go live with the Arab Monetary Fund's ‘Buna’, known as the Middle East’s new clearing and settlement payment platform, enabling financial institutions and Central Banks to send and receive cross-border multicurrency payments in a safe, cost-effective, risk-controlled and transparent manner. It aims to be the payment platform of choice, across the Arab world and beyond, by providing real-time payment solutions that empower Arab economies and promote greater regional integration. By joining the platform, Buna will offer DIB a unique value proposition, notably safe and affordable products, including retail and interbank transfers and remittances.

- In line with its sustainability strategy and strong commitment towards UAE's long-term green agenda, DIB announced its participation as a Key Partner in the citywide sustainability campaign "Dubai Can". The initiative aims to educate the society on making necessary changes to reduce waste and protect the environment, while providing access to free and safe drinking water across the city, and cutting back on the use of single-use plastic water bottles. This partnership is in line with DIB's sustainability strategy and showcases the bank's efforts in integrating sustainability and climate risk into its operating models, in order to ensure that the bank and its stakeholders are safeguarded against larger environmental concerns that are impacting the global economies today.

- Executing on our digital strategy, DIB WhatsApp was launched, where all DIB customers can enjoy the convenience of banking 24x7 via their favourite messaging app. The app is highly intuitive, easy to use, safe and secure with end-to-end encryption. The app offers wide range of banking services including, Salary in Advance, Credit Card payments, Account and Credit Card balance view, information on outstanding finance installments, subscription to IPOs and many more.

- DIB Consumer Banking launched it’s five year customer experience strategy in early 2022. Underpinning this strategy which is aligned to the ICARE values are some key critical initiatives such as ICARE training for front line staff, Customer experience masterclass for leadership, Service Reward and Recognition programme branded as Customer Happiness Heroes, monthly customer financial and inclusive awareness campaigns as well as Voice of Customer. In addition, DIB recently introduced the Customer Charter #AllAboutYou, which reflects the bank’s commitment in providing customers with banking services that are simple to understand, delivered in a responsible manner and in accordance with the highest standard of integrity.

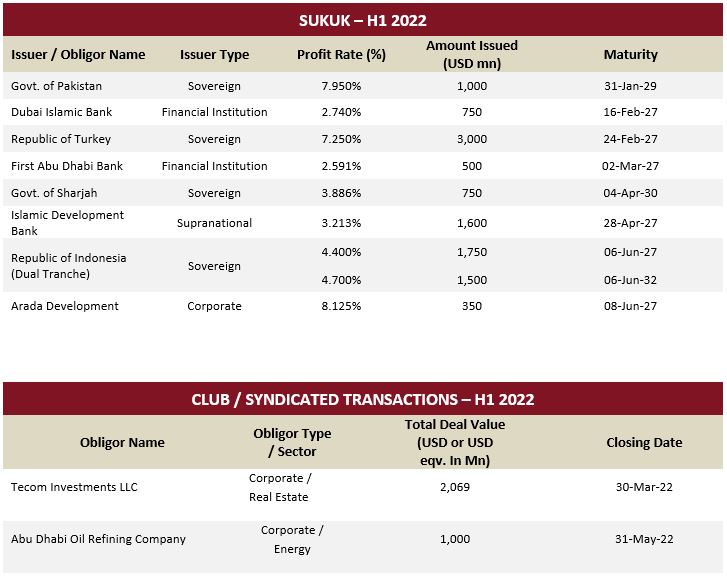

H1 2022 DCM and Syndication Deals:

DIB H1 2022 Awards List: