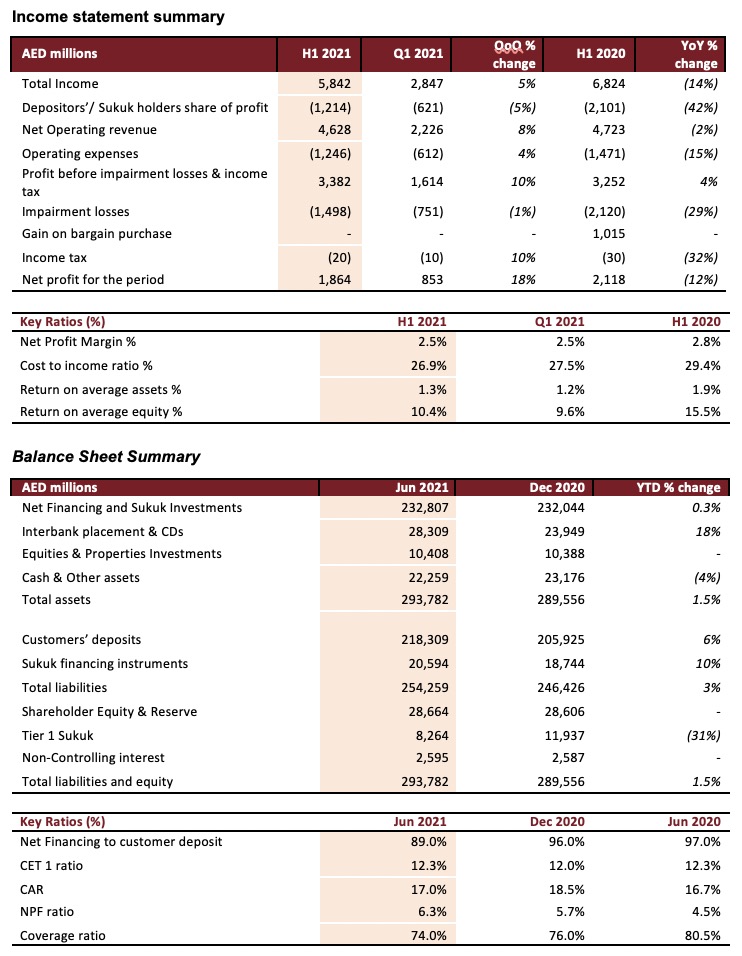

- Improving profitability with total income of AED 5.8 bln and net profit of AED 1.9 bln, up 5% and 18% QoQ respectively.

- Net operating profit before impairments reaches AED 3.4 bln, up 4% YoY and 10% QoQ.

- Robust growth in customer deposits of 6% year to date to reach to AED 218.3 bln.

- Efficiency build up continues with OPEX declining by 15% YoY to AED 1.2 bln.

- Sector leading cost income ratio of 26.9%.

Dubai Islamic Bank (DFM: DIB), the largest Islamic bank in the UAE and the second largest Islamic bank in the world, today announced its results for the period ending June 30, 2021.

First Half 2021 highlights:

- Total income increased by 5% QoQ to reach AED 5.8 billion YTD despite the challenging economic environment.

- Robust growth of 8% QoQ in net operating revenues now at AED 4.6 billion YTD, supported by low cost liquidity.

- Strong cost discipline led to further significant reduction in operating expense, down nearly 15% YoY from AED 1.47 billion to AED 1.25 billion.

- Impairment charge lower by 29% compared to same period last year, denoting improving credit quality trend.

- Net profits on an improving trend with an 18% QoQ jump to reach AED 1.9 billion YTD as a result of strong cost management, continued core income growth and lower impairment provisions.

- Earning assets remained stable with net financing and sukuk investment at nearly AED 233 billion despite significant corporate prepayments.

- Strong growth of 6% in customer deposits now at AED 218.3 billion, supported the balance sheet growth of nearly 1.5% to AED 293.7 billion.

- With CASA at a significant 41% of deposit base, liquidity remain strong with finance to deposit ratio of 89% and LCR of 152%.

- Healthy quarter on quarter improvements on ROA and ROE now at 1.3% and 10.4% respectively.

- Capitalization levels remained comfortably above minimum regulatory requirements, with CET1 at 12.3% and CAR at 17.0%.

Management’s comments for the second quarter ending June 2021:

His Excellency Mohammed Ibrahim Al Shaibani

Director-General of His Highness The Ruler’s Court of Dubai and Chairman of Dubai Islamic Bank>

- As the world slowly comes out of the shadows of the pandemic, the GCC region is well on its way to return to normalcy. UAE in particular has been phenomenal in the way it has managed the COVID-19 situation, right from the time it erupted until today, when the country holds the proud distinction of having administered the most vaccines in the world per capita. Based on the guidance of the leadership, the UAE has worked hard to ensure recovery during the first half of the year in key economic sectors such as travel, tourism and real estate with consumers and investors maintaining their confidence in the UAE’s successful pandemic response. At DIB, we remain optimistic of the continued positive outlook in the months to come and look forward to unequivocally supporting the major UAE events lined up for this year.

- This year is special for all of us in the UAE, citizens and residents alike, as we celebrate 50 glorious years of this young progressive nation. For a country still in its first half a century of existence, the United Arab Emirates is recognized today as the fastest growing nation in the world – it is a matter of great pride for DIB to be part of this journey all through the bank’s more than 45 years of existence.

- DIB’s core revenue generation has been on a steady positive trend since the peak of the pandemic with reported figure of AED 5.8 billion during the first half of 2021. This was a 5% increase over the previous quarter clearly depicting the bank’s resilience to and the robust strategy adapted in a challenging and changing environment.

Abdulla Ali Obaid Al Hamli

Board Member and Managing Director

- Dubai Islamic Bank’s commitments to impacted customers remained strong during the first half of the year with total instalment deferrals now reaching AED 9.5 billion across more than 54,000 customers. These relief measures are part of our strategy to ensure that economic activities in the UAE remains sound as the country gears up for one of the fastest economic recoveries in the world.

- With the introduction of DIB’s new business banking proposition, our customers whose businesses are now returning to normalcy, can benefit from further enhanced experiences and services across all the delivery channels reinforced by a robust digital platform in place.

- The re-energized dynamic values of the organization focused on customer care are going to be the key driving force for the bank in 2021 and the years to follow. This strategy is aimed at enhancing DIB’s customer acquisition across all major segments, both on the consumer and corporate banking side.

Dr. Adnan Chilwan

Dubai Islamic Bank Group Chief Executive Officer

- DIB’s profitability remained strong despite the challenging last eighteen months, with a net profit of AED 1.9 billion during the first half of 2021. Driven by stronger top line growth (due to volumes) and declining impairments trend, DIB remains on the planned steady recovery path the bank has outlined in its strategy . The first half of the year also saw a strong 18% rise in net profits over the previous quarter, as our core businesses witnessed a steady recovery and operational efficiencies buildup continues. The balance sheet is poised for further enhancement in net margins in line with any increase in interest rates in the markets.

- Funding and liquidity continue to be a strength of the bank with customer deposits growing by 6% YTD to now reach AED 218 billion. With LCR remains well above regulatory requirement at 152%, customer deposits continue to remain our prime source of funding, now accounting for more than 70% of the total base. This indicates DIB’s ability to raise liquidity almost at will to support the credit growth.Alternate sources of funding also remain open for DIB despite the challenging global environment as evidenced by the latest sukuk issuance of USD 1bln at a lowest ever pricing of 1.959% which was subscribed 3 times.

- With integration synergies fully realized, our focus on cost management continues to drive the bank’s operational efficiencies with cost income ratio now at a sector leading 26.9% and OPEX seeing a decline of 15% YoY.

- We remain committed to applying digital tech in every aspect of banking. From product offering to servicing, extensive changes are being put in place with the introduction of new tools and initiatives with a singular focus to make remote banking easier for our customers.

- The global pandemic has further underlined the importance of sustainability. We believe ESG to be an integral part of our long-term strategy to create and unlock further value for us as well as the industry we operate in. Today, our vision, purpose and values are fully aligned with the bank’s sustainability journey ensuring that our people remain committed to delivering on the promise of sustainable economic growth and prosperity

Financial Review:

Operating Performance

The bank’s total income in the first half of 2021 grew by 5% QoQ to reach to AED 5,842 million. The steady increase in total income over the past few quarters reflects the gradual re opening of the economy and business activities supported by well-managed vaccination rollout across the emirate whilst adhering to pre cautionary safety measures. Net operating revenue, however remained largely stable year on year to reach AED 4,628 million.

Operating expenses declined to AED 1,246 million compared to AED 1,471 million in the same period of last year, an improvement of over 15%. The reduction in operating expenses is attributed to the continued integration synergies achieved as well as a disciplined approach to cost management. The lower expenses have led to an improvement in cost to income ratio by nearly 250 bps year to date, which now stands at 26.9% vs 29.4% for FY2020, clearly a market leading position on this metric.

As a result, pre-impairment profit during the first half increased by 4% YoY and 10% QoQ reaching to AED 3,382 million compared to AED 3,253 million in the same period of last year.

Impairment charges declined by 29% year on year to AED 1,498 million, reflecting the bank’s continued prudent approach to underwriting risk given the current market conditions.

The net profit of the bank for the first half of 2021 reached to AED 1,864 million. The bank has sustained a strong growth of 18% on a quarterly basis despite the subdued operating environment.

Net profit margin continues to be stable at 2.5% despite the low-rate environment. ROA and ROE continue to remain healthy at 1.3% and 10.4% respectively.

Balance Sheet Trends

Net financing & Sukuk investments remained stable at AED 232.8 billion in the first half of 2021, despite early settlements from large corporates during the first half amounting to more than AED 8 billion. Sukuk investments now stands at AED 38.5 billion depicting a YTD growth of 9%.

Customer deposits increased to AED 218.3 billion in the first half of 2021, from AED 205.9 billion at year-end 2020 reflecting a robust rise of 6% YTD. CASA now stands at AED 90.2 billion representing about 41% of customer deposits. Liquidity coverage ratio (LCR) at 152% remains well above regulatory requirement which along with the finance to deposit ratio of 89% denotes an extremely healthy liquidity position.

Non-performing financing (NPF) ratio stood at 6.3%, with impaired financing at AED 13.1 billion vs AED 12.1 billion in end of 2020. The coverage ratio stands at 74% and overall coverage including collateral at 103%. Cost of risk on gross financing assets continue to be on a downward trend and now stands at 103 bps compared from 137 bps in year-end 2020.

Capital ratios continue to be stable with CAR ratio at 17.0% and CET 1 ratio is stable at 12.3% during the first half of 2021, both well above the regulatory requirement.

Business Performance

The bank’s business model remains well diversified with consumer banking contributing 36% to the bank’s H1 2021 net operating revenue whilst the corporate banking generated 40%. The latter continues to be the largest business segment within DIB comprising nearly 50% of the bank’s asset base followed by consumer and treasury combined at to about 31% as of H1 2021.

Gross new consumer financing of more than AED 6.5 billion during the first half was achieved driven by a healthy growth in the mortgage and personal financing portfolio while another AED 12 billion came from corporate.

A new business banking proposition was introduced during the quarter which provides a suite of variants for a diverse range of clients and customers from small businesses to medium-sized establishments. The proposition is also designed to evolve and provide complete digital eco-system to the SMEs in the UAE in order to become the transactional bank of choice.

In June, the bank successfully closed the lowest priced USD 1 billion senior sukuk which was 3x oversubscribed. The landmark success is a testament to the bank’s strong credit profile and standing with the international and regional investors.

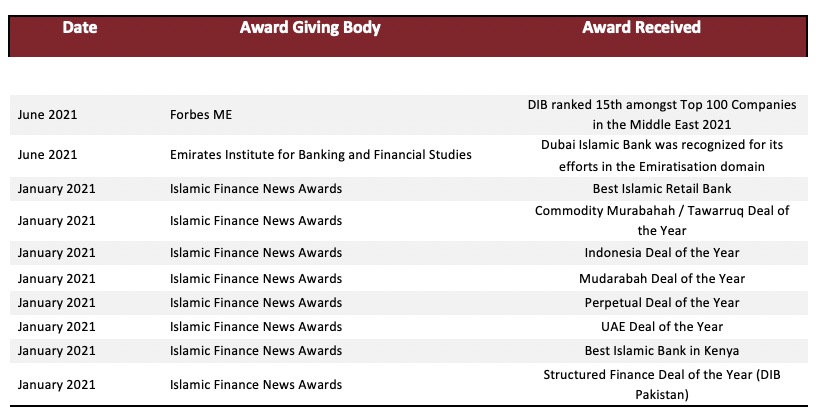

Year to Date Industry Awards (2021)