Dubai Islamic Bank Group Year End 2014 Results

Dubai Islamic Bank (DFM: DIB), the first Islamic bank in the world and the largest Islamic bank in the UAE by total assets, today announced its results for the year ended December 31, 2014.

Results Highlights

Resilient profitability stemming from growth in core business:

- Net Profit for the year 2014 increased to AED 2.80 billion, up 63% compared to AED 1.70 billion for 2013.

- Gross Revenue increased to AED 6.3 billion, up 20% from AED 5.3 billion for the year 2013.

- Net operating revenue increased to AED 5.6 billion, up 32% from AED 4.2 billion for 2013 on account of growth in core business.

- Net operating profit before impairment stood at AED 3.52 billion, up 38% from AED 2.55 billion for 2013.

- Cost to income ratio improved from 39.9% in 2013 to 36.7% in 2014.

Strong growth in earning assets across all business segments:

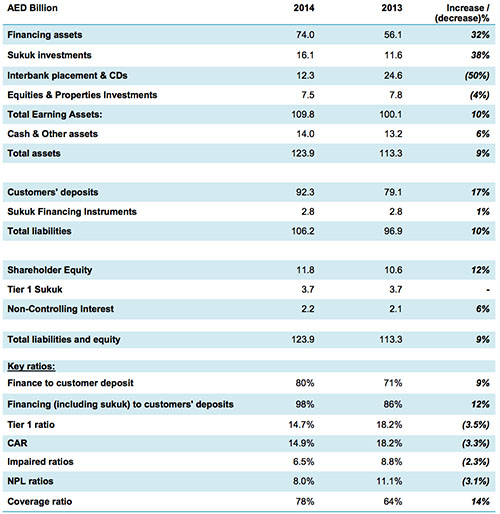

- Net financing assets at AED 74 billion, up by more than 32% compared to AED 56 billion at the end of 2013.

- Sukuk investments increased to AED 16.1 billion compared to AED 11.6 billion at the end of 2013, an increase of nearly 38%.

- Total Assets up by 9% at AED 123.9 billion compared to AED 113.2 billion at the end of 2013.

Improvements in asset quality

- NPLs on a consistent decline with NPL ratio improving to 8.0% at end 2014 compared to 11.1% at the end of 2013.

- Impaired financing ratio also improved to 6.5% at end 2014 from 8.8% at the end of 2013.

- Provision coverage improved to 78% at end 2014 compared to 64% at the end of 2013.

Strong growth in customers’ deposits

- Customer deposits up by 17% to AED 92.3 billion at end 2014 from AED 79.0 billion at end of 2013.

- Low cost deposits continue to remain a significant chunk with a large and stable CASA book comprising 45 % of total deposit base.

Strong Capitalization and liquidity position

- Capital adequacy ratio at 14.9%, as against 12% minimum required.

- Financing to deposit ratio is at 80%, one of the strongest in the market.

- Post year end 2014, additional T1 of USD $1 billion issued successfully raising overall CAR to 18.5%.

Significantly enhancing value for shareholders

- Earnings per share increased from AED 0.38 in 2013 to AED 0.61 in 2014.

- Return on assets improved by 74 bps from 1.62% in 2013 to 2.36% in 2014.

- Return on equity improved by 410 bps from 13.8% in 2013 to 17.9% in 2014.

DIB Board of Directors recommends the distribution of a cash dividend of 40%, subject to general assembly approval.

Financial Review

Income Statement highlights:

Total revenue

Total revenue for full year 2014 increased to AED 6,368 million from AED 5,288 million in 2013, an increase of 20.4%. The increase is mainly due to significant growth in core business related financing activities across both wholesale and consumer segments. With escalating positive customer sentiments and the intense customer penetration drive as part of the strategy to gain market share, corporate business has seen a surge in all areas resulting in higher funded and non-funded income. Consumer banking operations continue to expand delivering strong funded and fee income growth. Overall fees and commissions have increased by 49% to AED 1,189 million for the year ended 2014 from AED 799 million in 2013 largely due to a focused agenda to increase DIB’s share of wallet in 2014 in both corporate and consumer banking segments. Fee to net funded income increased to 21% from 19%.

Net revenue

Net revenue for the period ended 2014 amounted to AED 5,569 million, an increase of 31.5% compared with AED 4.2 billion in the same period of 2013. The increase in net revenue is mainly due to growth in core business coupled with savings achieved due to early settlement of high cost funding using bank’s surplus liquidity. Despite intense competition and aggressive pricing seen in the market, the bank was able to improve the net funded income margin to 3.57% from 3.34%.

Operating expenses

Operating expenses increased by 21% to AED 2,044 million for the year ended 2014 from AED 1,689 million in 2013 driven by growth in business activities. This resulted in cost to income ratio improving to 36.7% from 39.9% in 2013.

Impairment losses

DIB continues to strengthen its balance sheet by prudent lending and a conservative provisioning approach.

Despite notable improvement in asset quality, the bank built further provisions during the current period leading to a marked improvement in coverage ratio, which now, stands at more than 78%. Backed by strong collateral, the overall coverage including collateral at a significant discount or distressed value stands at nearly 134%.

Profit for the period

With significant increase in net revenue and improved asset quality leading to declining impairment charges, net profit for the year ended 2014, increased to AED 2,804 million from AED 1,718 million in 2013, an increase by 63%.

Statement of financial position highlights:

Financing portfolio

Net financing assets grew to AED 74 billion for the year ended 2014 from AED 56 billion at end of 2013, an increase of 32%. Consumer banking gross financing assets increased by 22.9% to AED 32.2 billion in 2014 compared with AED 26.2 billion in 2013. Corporate banking gross finance grew strongly by 36.3% to AED 46.9 billion in 2014 compared with AED 34.4 billion in 2013.

Non-performing assets have shown a consistent decline with NPL ratio improving to 8% for the year ended 2014 compared to 11.1% at the end of 2013. Impaired financing ratio also improved to 6.5% in 2014 from 8.8% at the end of 2013. This is mainly due to reduction in absolute NPLs coupled with increase in overall performing assets. Provision coverage improved to 78.1% in 2014 compared to 64.0% at the end of 2013.

Consumer Banking

The bank embarked successfully on an effective customer acquisition drive supported by enhancing manpower on the sales side over the past year. With more products to sell and a growing payroll account base, cross sell ratio has seen a strong upside during 2014. Whilst the consumer financing growth has witnessed a rise of more than 23%, the deposit momentum also continues unabated with an increase of more than 6% due to both new customer acquisition and existing customer enhancements. As such DIB today enjoys one of the strongest liquidity positions in the sector.

Wholesale Banking

The wholesale and corporate banking has been a key area of financing assets growth in 2014. A focused sales approach combined with a more comprehensive product and service offering allowed the bank to not only deepen its existing relationship and successfully enhance its share of wallet of current wholesale clients, but also facilitated entry into new sectors and segments, previously untapped by the bank. These include healthcare, education, hospitality, tourism, logistics and free zones, amongst others. Simultaneously, while continuing its advancements within the emirate of Dubai, the bank has successfully diversified its corporate business in other emirates as well with non-Dubai now contributing significantly to the growth of the financing book.

Sukuk Investments

Sukuk investments increased by 38% in 2014 to AED 16.1 billion from AED 11.6 billion at end of 2013, as part of a deliberate strategy to deploy excess liquidity in higher earning assets. Primarily a UAE based portfolio including sovereign and non-sovereign names, this provides a strong yield and can also be used to generate liquidity through repos and other mechanisms if and when required by the bank.

Customer Deposits

Customer deposits for the year ended 2014 increased by 17% to AED 92.3 billion from AED 79.1 billion as of 2013. And though the customer deposits have grown, CASA continues to be a significant portion comprising 45% of total deposits amounting to AED 41.9 billion for the year ended 2014 compared with AED 33.8 billion in 2013, giving rise to one of the lowest cost of funds in the market and allowing the bank to compete effectively whilst maintaining and improving margins.

Investment deposits have also grown by 12% in 2014 to AED 50.4 billion from AED 45.2 billion in 2013. The increase in customer deposits is in line with the growth in investing and financing assets leading to a financing to deposit ratio of over 80% at the end of 2014.

Capital and capital adequacy

Capital adequacy ratio stood at 14.9% for the period ended 2014. Tier 1 CAR stood at 14.7 % with both overall CAR and Tier 1 well above the required regulatory level. Subsequent to the year-end, DIB has successfully concluded issuance of T1 capital amounting to USD $1 billion which resulted in increasing CAR to 18.5%

Key successes for the year 2014:

- DIBs “SMART Bank” strategic initiative has redefined the bank’s customer service and created a new standard and benchmark across the UAE. Aligned with Dubai’s “Smart City” agenda, the bank is eyeing new frontiers in customer experience. This innovative platform will serve the growing demand for banking services by allowing customers to complete their banking transactions at DIB branches electronically through an entirely seamless process with faster turnaround times. New customers can now complete their account opening formalities and walk out with their instantly issued ATM cards and cheque books within 15-20 minutes. System integration with the Emirates Identity Authority enables uploading of customer information directly from the Emirates ID cards into the Bank’s systems. Customer transactions are completed without filling forms using handheld electronic devices with digital signatures taken for secure and efficient processing.

- In June 2014, DIB completed the acquisition of 24.9% shares in Bank Panin Syariah in Indonesia. DIB intends to finalize the acquisition with enhancing the stake to 40% and then establishing a new growth agenda in this highly attractive and one of the largest Islamic markets in the world.

- 2014 has seen the bank penetrate into many new and previous untapped segments. Further, the corporate financing book grew by 39% in 2014 in line with supporting key economic sectors such as airlines, power & energy, retail, manufacturing & services, etc.. Corporate relationships were also deepened with enhanced penetrations leading to larger share of wallet.

- Earlier during the year, DIB enhanced its foreign ownership limit to 20% based on increasing demand. This decision allowed the bank scrip to become a major component of the MSCI basket whilst also becoming one of the most actively traded stocks on the DFM in the year 2014.

-

Throughout the year, new products and services were launched such as:

- DIB tie up with All Funds International offering customers investment opportunities in a range of Shariah-compliant funds.

- Launch of Secured Share Finance, a unique facility to finance Sharia-compliant securities traded on the Dubai Financial Market (DFM), Abu Dhabi Securities Exchange (ADX) and NASDAQ Dubai.

- Prime Cards based on the principle of Salam. The Prime Cards product family comprises Infinite, Signature, Platinum, Gold and Classic cards.

- Special Auto Takaful Plan in partnership with Dubai Islamic Insurance & Reinsurance Co. (AMAN) with low premiums, maximum coverage and easy payment plans.

- Salam Finance (Based on Salam contract) for non-individuals (businesses).

- Launch of Liability Settlement Finance - this Personal Finance product offers a “One Payment Solution for all your debts”, whereby a customer can combine all his/her debts into one easy finance solution.

- Wakala Deposit product for individual and SME customers. This product offers customers upfront expected profit rates with a choice of investing in tiered investments across tenors. Moreover, the Wakala allows customers access to profits immediately upon maturity or early redemption.

Management’s comments on the financial performance of the financial period:

His Excellency Mohammed Ibrahim Al Shaibani, Director-General of His Highness The Ruler’s Court of Dubai and Chairman of Dubai Islamic Bank, said:

- 2014 has been an exceptional year for the bank as evidenced by its strongest results in the bank’s history with full year net profits reaching AED 2.8 billion, an increase of 63% compared to 2013.

- The strong results have been achieved despite challenging conditions in the latter part of the 2014 around oil price and equity market volatility.

- Dubai is strongly positioned to withstand the current volatilities in the oil market given its diversified economy and infrastructure and DIB’s 2014 performance echoes the bank’s strategic alignment to support the growth agenda of the Emirate as well as its ambitions to become the global capital of Islamic economy.

Dubai Islamic Bank Managing Director, Abdulla Al Hamli, said:

- The strong positive results for the year 2014 is a testament to the bank’s capabilities in the current macro-economic and business landscape.

- Throughout the year, DIB have continued to progress in the industry through launching award winning products and services focused on benefitting our customers.

- The bank’s successful and active participation in supporting this year’s high level summit “The 10th World Islamic Economic Forum” in Dubai has further strengthened the institution’s franchise in the Islamic world and DIB is now seen as one of the leading Islamic banks with a growing international footprint.

Dubai Islamic Bank Chief Executive Officer, Dr. Adnan Chilwan, said:

- We started 2014 with a well-defined growth agenda marking the end of the consolidation phase running from 2009 to 2013. The successful execution of this consolidation phase resulted in a robust platform allowing the bank to seamlessly switch gears.

- Despite the relatively subdued market, the bank has witnessed a 63% hike in net profit and 32% jump in financing book compared to the same period last year, and all stemming from regular, core and normal banking activities .

- We are now looking beyond just the financials. Our deliberate and focused growth strategy and unconventional approach has led to an organizational transformation where every employee strongly believes that our potential is limitless.

- Customer centricity and relentless innovation forms the core of our strategic agenda providing us with an unparalleled edge in the industry, and setting the standard for others to follow.

- We have redefined service across the UAE market with the “SMART BANK” launch reinforcing our customer focus around selling satisfaction rather than products, and keeping banking simple.

- Global economic growth and development has seen a major shift over the last decade with Asia and in particular, Middle East, South Asia and Far East being amongst the major drivers. In most of these high growth nations, Islamic Finance is essentially being seen as a key component of economic progress and prosperity which in turn, has led to substantial enhancement of wealth across a growing population fuelling massive liquidity within the Islamic investor base.

- As the world’s first Islamic bank, we at DIB shoulder the responsibility of developing this fast growing segment into a global norm for banking and finance.

- Moving towards 2015 as the franchise celebrates its 40th year anniversary, we look forward to continuing the momentum we have built so far leading the institution to new frontiers of excellence and supporting not only the development and growth of Islamic finance but also the aspirations of the nation and all our stakeholders.

Full Year 2014 Awards